The moment you hand a fintech codebase to an external partner, three things leave your control: the source code, the credentials and secrets that let it run, and the customer financial data it touches. Once any of those crosses the boundary, getting them back is a contract dispute, a security incident, or a regulatory submission, never a quick fix. The protections that matter are the ones you write into the agreement before the transfer, not the ones you negotiate after something has gone wrong.

The stakes have moved sharply in 2026. IBM’s 2024 breach report puts the average financial-sector breach at USD 6.08 million, roughly 22% above the global average. The EU’s DORA regulation, in force across the European financial sector since January 2025, now puts ICT third-party service providers directly inside the regulator’s oversight scope. And PCI DSS v4.0.1 became fully mandatory on 31 March 2025, with continuous validation now the expected default. Choosing a fintech software development company is no longer a procurement decision; it’s a compliance decision with a six-figure to multi-million-dollar downside if you get it wrong. From our delivery experience at Ariel, the engagements that hold up are the ones where the buyer is locked in the right protections before the first commit.

Here is what to demand from any fintech development partner before your code, keys, and customer data leave the building.

Key Takeaways

- Regulatory scope has shifted. Under DORA, your vendor’s failures are your regulatory exposure. The vendor selection is now a compliance check, not just a procurement decision.

- The protections that matter are the ones at the moment of transfer: source-code custody, secrets handling, data residency, and IP assignment. Negotiate them before the first commit.

- PCI DSS v4.0.1 is fully mandatory in 2026. The vendor’s secure SDLC, scripted-page integrity, and stronger authentication discipline are non-negotiable for any payment-data workflow.

- SOC 2 Type II and ISO 27001 are baseline assurance, not replacements for PCI DSS, DORA, or GDPR. Verify the actual reports, not website badges, scoped to the delivery organization.

- Fintech-fluent engineers cost 20% to 35% more than generalist developers. That premium reflects scarcity and risk, not margin.

- The five protections that matter most: data-flow scoping, source-code custody, secrets governance, secure SDLC artefacts, and audit-ready exit terms.

- The cheapest place to catch a vendor risk is in the contract. The most expensive is in the breach notification.

Why Fintech Vendor Selection Is Now a Compliance Decision

Generic vendor evaluation guides treat the development-partner choice as a capability question: can this team build what we need. For fintech, that framing now under-scopes the decision by a wide margin. DORA, in force across EU financial entities since January 2025, explicitly extends regulatory accountability to ICT third-party service providers. The European Banking Authority oversees critical third-party providers directly. That means a development partner’s security failure can produce a regulatory finding against your firm, not just a vendor dispute.

PCI DSS v4.0.1 raised the bar on the technical side. Scripted-page integrity, change and tamper detection on every payment page, stronger authentication rules, and the customized approach to continuous validation are all in force. Picking a fintech software development company that treats these as audit-prep rather than platform properties is a budget risk in disguise; the team will spend project hours retrofitting controls that should have been built in from sprint one. And the cost of getting it wrong is real: IBM’s 2024 data puts the financial-sector breach average at USD 6.08 million, a number that has grown every year since 2021.

The pattern across all of this is consistent. Fintech development is no longer ordinary software development with extra paperwork. It’s a regulated activity where the contract you sign with your fintech software development company partly determines your regulatory posture, and the protections you demand before the transfer determine whether the engagement holds up under scrutiny.

The Five Protections to Lock In Before the Transfer

These five protections, written into the contract before any code or credential crosses the boundary, prevent the failures that show up later as incidents, regulatory findings, or expensive exits. Run all five on any fintech software development company you’re seriously considering for fintech app development services.

1. Data-flow scoping (defines what the vendor can actually touch)

Most fintech breaches involve data the vendor never needed access to in the first place. The first protection is a scoped data-flow agreement that names exactly what the vendor will see, store, transmit, or process. Anything outside that scope stays out of their environment.

- Inventory every system, database, and API the engagement requires access to.

- Define which environments contain real cardholder or PII data and which use synthetic or masked data.

- Restrict the vendor’s identity and access controls to the minimum required for delivery (least-privilege by default).

- Verify that the vendor’s environment can actually enforce the scope (network segmentation, data masking, vault-managed secrets).

2. Source-code custody (keeps the asset under your control)

Vendor-hosted code is one of the most common forms of fintech lock-in, and one of the most expensive to unwind during an audit or an exit. The fix is to make source-code custody a contractual property of the engagement from day one, not an afterthought at the end.

- Repository ownership. All code committed to a repository under the buyer’s GitHub, GitLab, or Azure DevOps organization, not the vendor’s.

- Source-code escrow. For critical workloads, third-party escrow that releases the code to the buyer on defined trigger events (insolvency, breach of contract, sustained delivery failure).

- Branch and access discipline. Vendor engineers have role-scoped repository access, not blanket admin; pull-request workflows enforced.

- IP assignment. Explicit assignment of code, derivative works, models, and any libraries created during the engagement to the buyer.

3. Secrets and credential governance (the breach-prevention layer)

Stolen or compromised credentials remain the highest-cost breach vector. The protection is operational discipline on how secrets are stored, rotated, and accessed across vendor and buyer environments. Vendors that manage secrets in shared spreadsheets, environment files, or chat-tool snippets are an active breach risk.

- All credentials, API keys, and tokens stored in a vault (HashiCorp Vault, AWS Secrets Manager, Azure Key Vault), never in code or environment files.

- Vendor engineers issued time-bound, role-scoped credentials with mandatory rotation.

- Secret scanning in CI to prevent accidental commits.

- Documented offboarding procedure for vendor team members rotating off the engagement.

4. Secure SDLC artefacts (the verification of how they actually work)

A fintech software development company can claim a secure software development lifecycle in any pitch deck. The verification is in the artefacts: real documents from real engagements that demonstrate the practice is built into the platform, not bolted on for the audit. The discipline of verifiable security and traceability extends well beyond fintech; the governance principles we apply when auditing AI agents share the same operational shape.

- Threat-modeling documentation for systems handling sensitive data.

- Recent penetration test results (redacted as needed) and remediation evidence.

- Tooling fluency across SAST, DAST, SCA, secret scanning, and SBOM generation.

- Engineer credentials in security-relevant areas (CSSLP, CISSP, OSCP, cloud security specialties).

- Evidence of prior PCI DSS, SOC 2, or DORA-relevant engagements, with named scope.

5. Audit-ready exit terms (the engagement-recoverable clause)

The protection most likely to be left out of an MSA template is the one that matters most when an engagement goes wrong. Exit terms decide whether you can recover the work, the data, and the operating system if you need to bring it in-house or move to a different partner.

- Defined exit window with explicit knowledge-transfer obligations: documentation, runbooks, architecture decision records.

- Data return and destruction with attestation, including from any sub-processors.

- Credential and key revocation on a defined timeline post-exit, verifiable by the buyer.

- Continued support obligation during transition, with pricing agreed in advance to prevent leverage at exit.

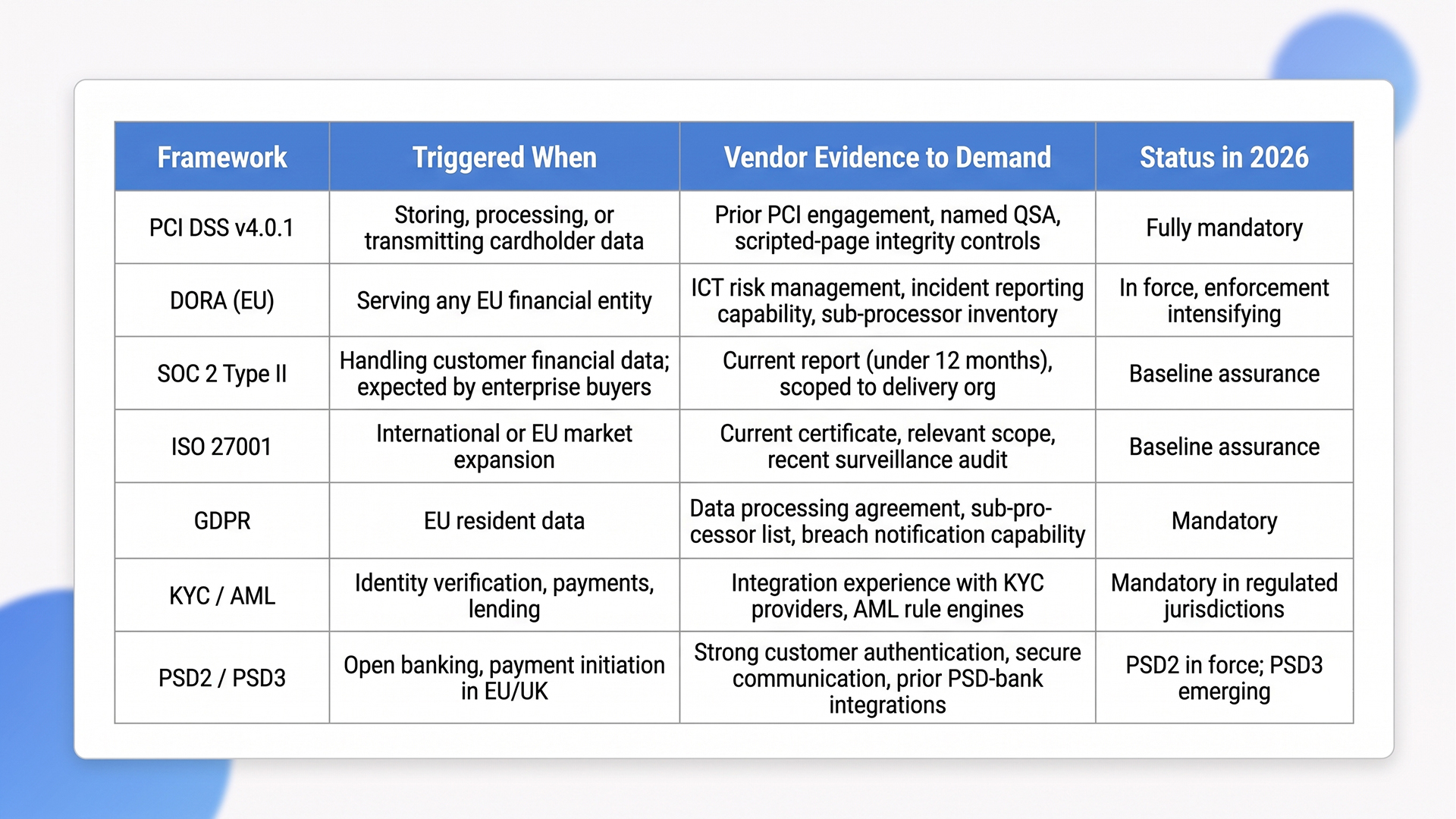

The Fintech Compliance Stack: What to Verify

Different fintech products trigger different compliance obligations. The table below names the most common frameworks, what triggers them, and what evidence to demand from any vendor responding to a fintech brief. Definitive scope questions for any regulated workflow should always involve qualified counsel rather than vendor assurances.

SOC 2 Type II and ISO 27001 are not replacements for PCI DSS, DORA, or GDPR. They are signals that a vendor has standard security controls, which is necessary but not sufficient. Verify the relevant framework certifications for your product directly, ask for the actual reports rather than badges, and walk away if the scope of those reports does not cover the delivery organization that will handle your work.

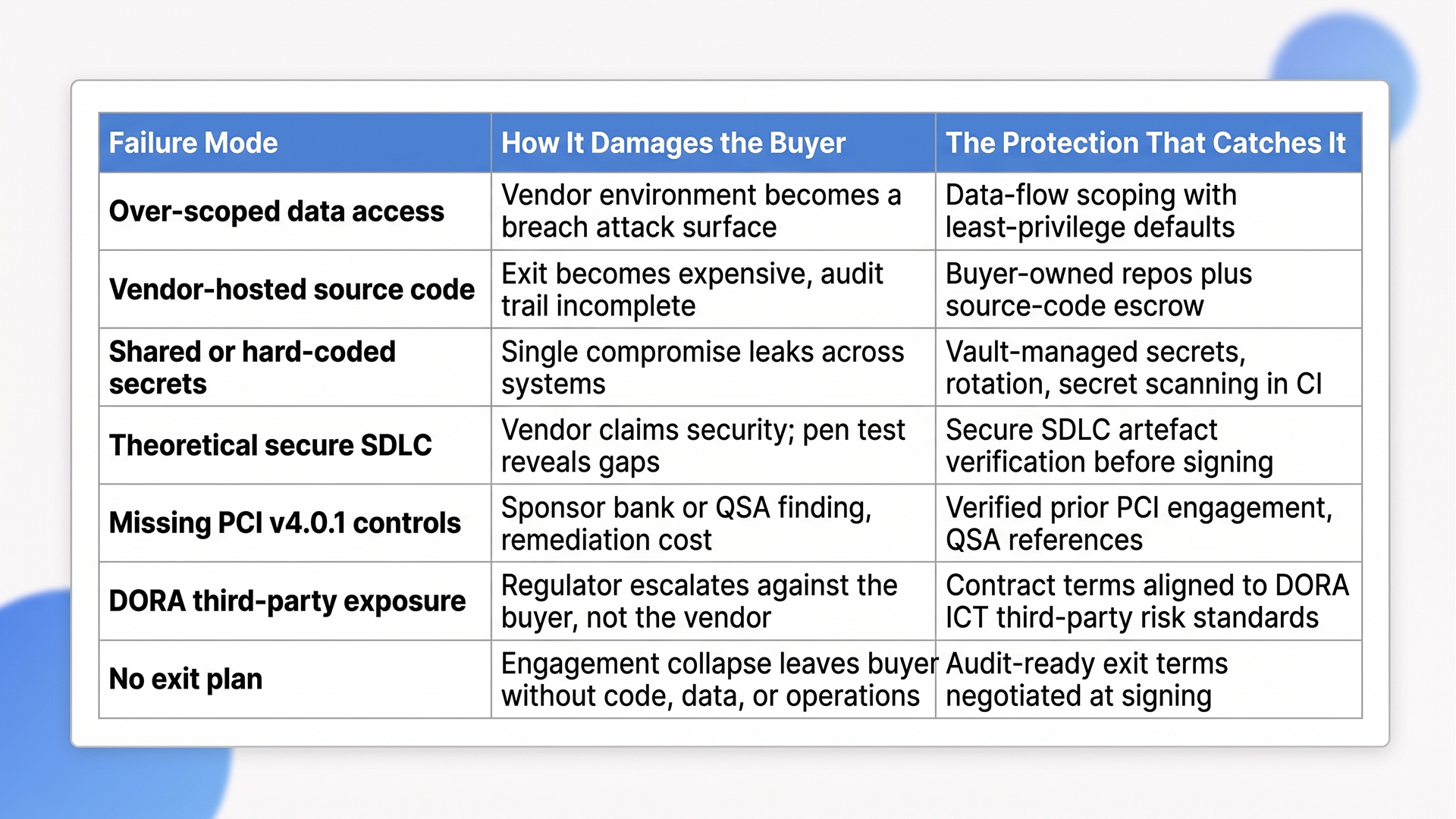

Where Fintech Engagements Break (and the Protection That Catches It)

From our delivery experience and the broader pattern across the fintech market, the engagements that fail concentrate around a small number of recognizable failure modes. Each maps to a specific protection from the list above.

When Hiring a Fintech Development Partner Is the Wrong Move

Even with strong protections, an external development partner is not always the right answer. Here is when we tell fintech buyers to wait or take a different path.

The capability is core to the regulated product. If a system is the regulated core of your fintech (the ledger, the KYC decisioning engine, the fraud model), the architectural judgment and operational ownership belong inside the company. Outsourcing the regulated core trades short-term speed for long-term dependency, and any future audit becomes harder.

Your data foundation isn’t audit-ready. If your data governance is fragmented or your audit trails are incomplete, any partner you hire to hire fintech software developers will inherit those problems and surface them at the worst possible moment. Fix the foundation first, then engage a partner. The pattern is the same one we examine in our breakdown of AI implementation challenges, where modern workloads break on legacy foundations.

You don’t yet have an internal security owner. Outsourcing fintech development without a named internal security lead means there’s no one inside your organization who owns the controls, the audit posture, or the vendor oversight. That gap will surface in a regulatory inquiry or a customer security review. Hire (or appoint) the internal owner before you hire the development partner.

The engagement is too small to justify the compliance overhead. For genuinely small or proof-of-concept work, the cost of compliance verification and contractual due diligence can exceed the engineering cost. A senior freelance fintech engineer or a short paid discovery can be the proportionate response. Reserve full vendor engagements for work where the budget at risk justifies the discipline.

How Ariel Approaches Fintech Engagements

From our delivery experience across regulated industries, the fintech engagements that hold up are the ones where the protections above were negotiated before the first sprint, not retrofitted after the first audit finding. We respond to fintech briefs regularly, and the buyers worth working with are the ones who ask for the secure SDLC artefacts, the named compliance experience, the IP and exit terms, and the secrets-governance discipline. The vendors worth hiring welcome that scrutiny.

The operating principles we apply across every fintech engagement, and that any buyer should expect from a serious fintech software development company, are:

- Data-flow scoping in week one. Least-privilege access from day one, with vendor environments segmented from any data the engagement doesn’t require.

- Buyer-owned repositories. All code under the buyer’s organization with role-scoped access for vendor engineers, plus source-code escrow for critical workloads.

- Vault-managed secrets and CI-level scanning. No credentials in code, no hard-coded keys, no secrets in chat tools.

- Compliance designed into the architecture. PCI DSS, DORA, and GDPR controls built into the platform from sprint one, not bolted on before the audit.

These same disciplines hold when fintech engagements include modernization of legacy core systems, which is increasingly common as banks and lenders move off aging stacks. The lessons from our legacy application modernization work apply directly: discovery before build, rollback paths at every stage, structured handover.

Evaluating a fintech development partner and want a delivery-grade read on the protections that actually matter?

Our team has scoped and delivered fintech engagements across regulated environments for 16 years. We’ll walk through your data-flow boundaries, source-code custody, secrets governance, compliance posture, and exit terms, then give you a verifiable read on what to demand before any code leaves your environment.

Frequently Asked Questions

1. What should I demand from a fintech software development company before signing?

Five protections, all written into the contract before any code or credential transfers. Data-flow scoping that limits the vendor to least-privilege access. Source-code custody under the buyer’s repositories with escrow for critical workloads. Vault-managed secrets governance with rotation and CI-level scanning. Verifiable secure SDLC artefacts (threat models, pen tests, named compliance engagements). And audit-ready exit terms with knowledge-transfer, data return, and credential revocation obligations. Have qualified counsel review the contract language before signing.

2. What compliance certifications does a fintech app development services partner need?

It depends on your product and market, but most fintech app development services engagements need at least three checks. SOC 2 Type II as baseline assurance, with the current report (not older than 12 months) scoped to the delivery organization. ISO 27001 if you’re serving European or international clients. And direct, evidenced experience with the framework your product actually triggers: PCI DSS v4.0.1 for card data, DORA for EU financial entities, GDPR for EU resident data, KYC/AML for identity-verification or payments work. Ask for the reports, not the badges.

3. How does DORA affect my vendor selection?

DORA, the EU Digital Operational Resilience Act, has been in force since January 2025 and explicitly extends regulatory accountability to ICT third-party service providers. In practice, that means a development partner serving an EU financial entity now sits inside the supervisor’s scope, and the financial entity is responsible for ICT third-party risk management. For buyers, the implication is direct: vendor selection is now a compliance check, the contract has to cover DORA’s ICT risk management obligations, and sub-processor inventories and incident reporting capability are non-negotiable.

4. How much more does it cost to hire fintech software developers compared to generalists?

When you hire fintech software developers or partner with a fintech-fluent team, expect a premium of roughly 20% to 35% over generalist development rates. The premium reflects scarcity (engineers with PCI, DORA, and payments-integration experience are limited) and risk (the cost of getting fintech work wrong, both regulatory and reputational, is higher). For payment-touching or regulated workloads, paying the premium is usually cheaper than hiring generalists and absorbing the compliance retrofit cost.

5. Should I use source-code escrow for a fintech engagement?

Yes for critical workloads, especially those that touch regulated data or could become operationally essential. Source-code escrow releases your code to you on defined trigger events (vendor insolvency, breach of contract, sustained delivery failure), so an engagement collapse doesn’t take your platform with it. The annual cost of an escrow arrangement is modest relative to the cost of being locked out of your own code in a regulator-watched scenario.

6. Can Ariel help us scope a fintech engagement?

Yes. We help fintech buyers scope engagements before any commitment, including the data-flow boundaries, compliance posture, contract terms, and exit obligations. The review is independent of whether we eventually deliver the work. Get in touch for a delivery-grade conversation about your specific use case.

The Transfer That Decides the Engagement

Choosing a fintech software development company is no longer a procurement decision with security implications. It’s a compliance decision with budget implications. DORA put your vendor’s failures inside your regulatory perimeter. PCI DSS v4.0.1 made continuous validation the baseline. The IBM data on financial-sector breaches puts the cost of getting it wrong in seven-figure territory. None of these are reasons not to outsource. They are reasons to be specific about what you protect at the moment of transfer.

Scope the data flow. Keep source code under your control. Govern secrets in a vault, not in code. Verify the secure SDLC with real artefacts, not pitch decks. Lock in audit-ready exit terms before signing. The protections are not exotic; the discipline of demanding them before the transfer is what separates the engagements that hold up from the ones that produce regulatory findings six months in.

Ready to engage a fintech development partner with the protections your codebase, your customer data, and your regulatory posture actually require?

Book a free consultation with Ariel’s fintech team. We’ll review your data-flow boundaries, your compliance scope, your contract posture, and the protections that have to be in place before any code or credential leaves your environment.